In the rapidly evolving landscape of banking and finance, harnessing the power of fintech is no longer an option but a necessity. Fast-moving fintech startups are outpacing traditional banks in terms of technological innovation and customer-centric solutions.

The banking industry is increasingly aware that building everything in-house is no longer viable for all but the biggest players. As a result, many banks are increasingly looking to partner with fintech companies to provide the technology solutions customers are looking for.

While it may feel like it's important to move quickly to set up such partnerships, banks need to perform due diligence on all potential suitors. Choosing the wrong partner could not only put your customers (and their money) at risk; it could damage the bank's reputation and potentially even ruin the business.

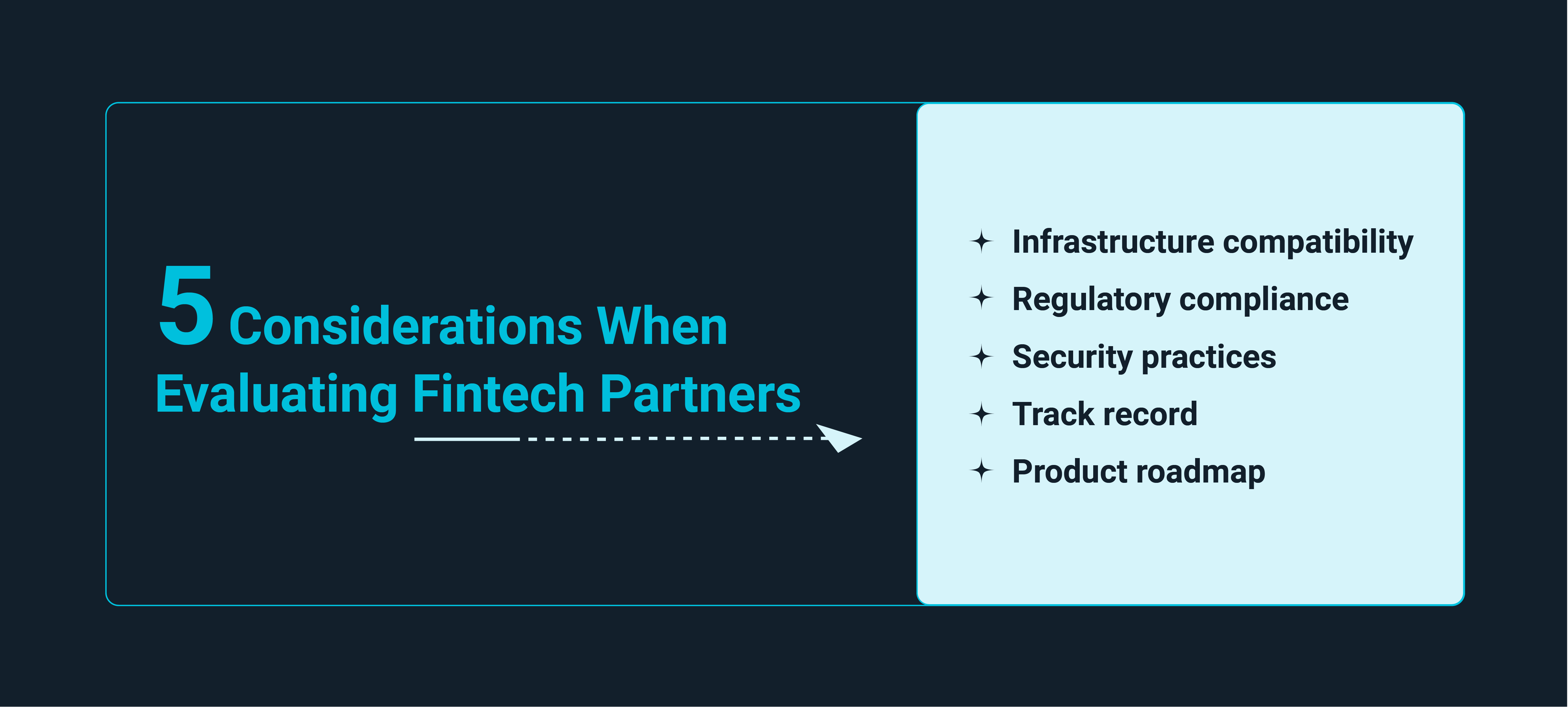

Here are some key aspects banks should look at when evaluating a prospective fintech partner:

Infrastructure Compatibility

The primary reason for a bank to partner with a fintech company is to leverage their technological prowess to add innovative capabilities to your service offerings. After reviewing their product to confirm that it looks and works as promised, your in-house technical team should perform an in-depth evaluation of compatibility with your existing infrastructure.

Ideally, their tools will already have integrations built for your bank's technology platforms that have been proven and tested. If custom-built integrations are required, find out if their team has experience working with your specific software or similar tools. Building custom integrations typically extends the implementation process, and the prospective partner should estimate how long it would take and appraise you of any potential risks.

Regulatory Compliance

While many would prefer this not to be the case, fintechs are subject to regulatory standards like other financial institutions. The specific regulations will vary based on the product offered -- payment providers are regulated differently than robo-advisors, for example. It is necessary to assess what regulations the potential partner is potentially subject to, that they are currently in compliance with these regulations, and that they have robust controls in place to ensure continued compliance in the future.

While there are segments of fintech that are not entirely regulated or where the regulation situation is unclear (e.g., crypto) that may be tempting or appealing, it's essential to understand the potential regulatory risks for your bank should you partner with a company in one of those spaces.

Security Practices

With cyber-attacks and data breaches increasingly common, evaluating a potential partner's security practices and infrastructure is important to ensure that your customer data will be protected. Be sure to examine their encryption methods, authentication protocols, and how they handle sensitive customer data. Additionally, it's worth looking into their incident response plan in the event of a data breach.

A good indicator that a prospective partner takes security seriously is a SOC 2 Type 2 certification. To earn this certification, a company has to undergo a comprehensive external audit of its security controls based on five Trust Services criteria: security, availability, processing integrity, confidentiality, and privacy.

Track Record

A fintech company with a proven track record in delivering successful results should be given priority. It is vital to look into their previous partnerships, customer testimonials, and case studies demonstrating their ability to deliver results. Websites like Capterra and G2 make it easy to find honest reviews of software products by current and former customers.

In the case of early-stage startups that may have a limited track record or customer base to build a verifiable reputation, look at the resumes of the founders and key team members to see if they have a record of growth and success. Who its board members, advisors, and major investors are will help you determine if the startup has a good chance of success.

Product Roadmap

The fintech landscape is continually evolving. Hence, evaluating the potential partner's adaptability and preparedness for future trends is essential. What their product roadmap looks like will help you understand the company's direction, what features you can expect during your contract, and whether any potential shortcomings in the existing product will be corrected within a reasonable timeframe. Additionally, a customer-centric fintech that adjusts its product plans based on customer feedback will make a better partner than one more resistant to change.

Transform Your Business Credit Program With PoweredBy

If your bank is looking to modernize its business credit offerings, we're here to help. We created our Powered By program to allow community banks and credit unions to provide their clients with a modern credit card and spend management product while avoiding the time- and resource-intensive project of building the technology in-house.

Built through work with SMB clients, the Torpago platform provides a single portal for all business credit card functions. We're SOC 2 certified and have integrations with over 1,000 software tools, so your customer data will be secure, and implementation within your infrastructure will be quick and painless. Request a demo today to learn more!